The Patient Protection and Affordable Care Act is a United States federal statute that was signed into law by President Barack Obama on March 23, 2010. The PPACA is aimed at creating state based Health Benefit Exchanges in the US. The Health Benefit Exchanges are expected to provide individuals and Small Groups (SG) access to affordable health insurance. The Congressional Budget Office predicts that by 2019, about 24 million people will have insurance through these exchanges.

Health Benefit Exchanges will make affordable health care available in a transparent manner. They will also accelerate the growth of the healthcare sector by presenting new opportunities for payers, providers and public health care administrators. Each state has been mandated to set up their Health Benefit Exchanges by January 2014. Understanding and meeting State and Federal compliance requirements will be the foundation for a faster go-to-market strategy.

Health Benefit Exchanges will transform the way individuals and Small Groups shop for health plans. They will function as aggregators, making standardized insurance plans easily comparable for individual and Small Groups buyers. The impact of the transparency will be a fall in insurance costs.

Ensuring transparency by enabling plan comparison in web portals is a fairly revolutionary idea in health care, but it is not a new business paradigm. For years, airline fares have been comparable on a variety of travel websites, ensuring that travelers can make well-informed choices. Health Benefit Exchanges will work in a similar manner. They make a wider and cheaper set of choices available to small healthcare buyers who earlier could not find the deals that large employers or groups enjoyed. By enabling choice for a wider spectrum of insurance buyers and equipping them with decision support tools, Health Benefit Exchanges can expect to increase sales and improve customer satisfaction levels. This contributes to a winwin situation for both buyers and providers.

The nature and structure of Health Benefit Exchanges will make a significant difference to:

Exchange operators (State or the Federal Government) will be pivotal to success. They will be responsible for delivering the guided buying experience, monitoring plan performance and quality ratings. They will also become responsible for the IT infrastructure of the exchange, data integration, and interoperable data exchange standards. In addition, operators will need to set up customer management and support infrastructure for phone-based exchange services.

The Exchange Operating Model has been left to the discretion of individual States. Each State can adopt a model from a variety of approaches:

Each State also has the latitude to decide the degree of regulation beyond PPACA they may wish to implement. This will position the states as Active Regulators or Passive Enablers

Health Plan Exchange Capability Model (To-be): Forcing Cost Leadership

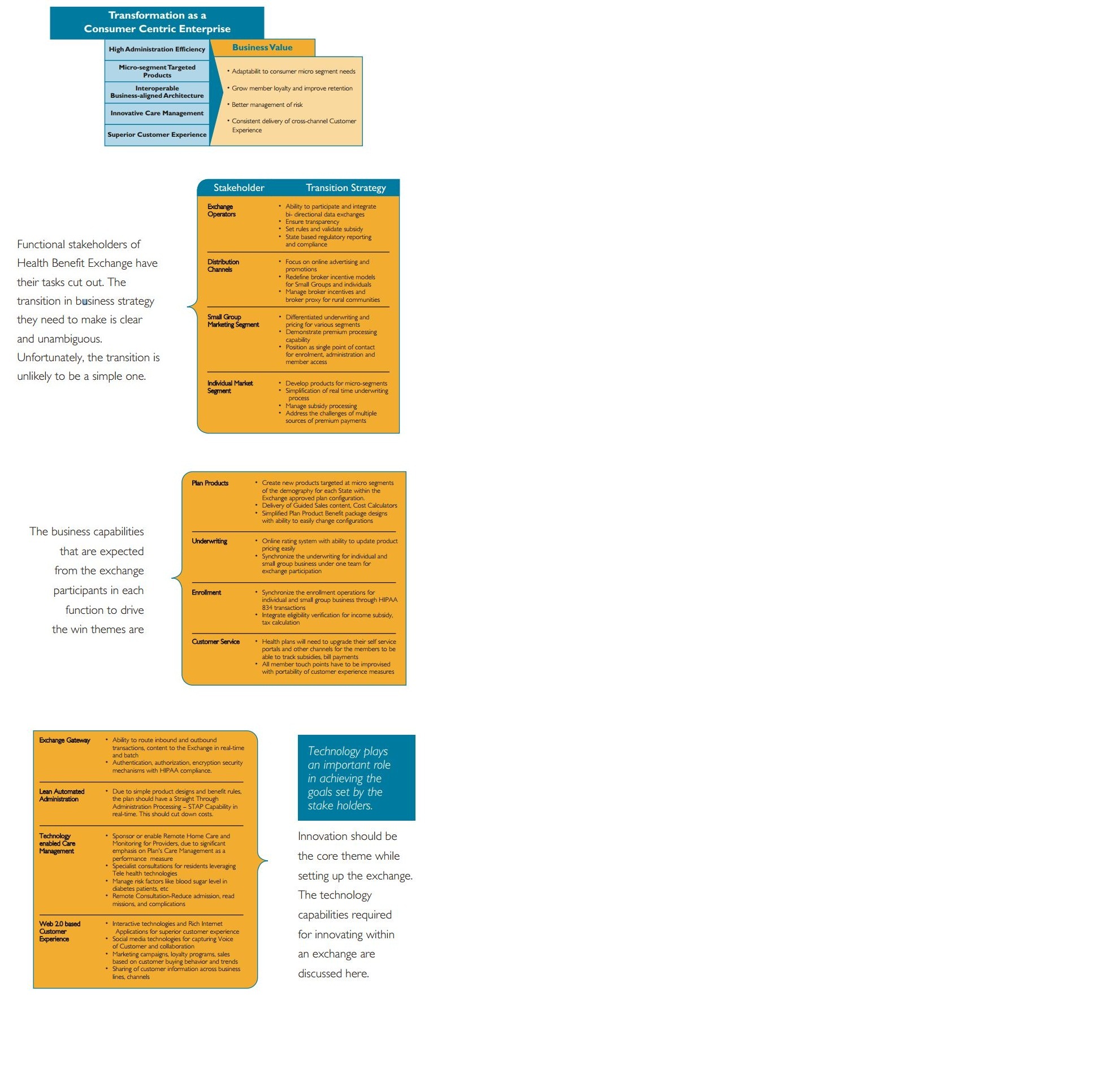

The PPACA mandate on health benefit exchanges has caused dilemma for most health insurance companies. The contour for decision making may differ from payers to payers. But the main concerns are on the following lines. Should health plans participate in an exchange-based model? If they participate, should it be in all States or selectively in a few States? If they don't participate, are they losing a large pie of prospective customers? Also, regardless of the number of States the health plans participate in, which are the best segments (subsidized individual, unsubsidized, small group etc.) to address? These choices will determine the to-be capability model each player must fulfill.

State Exchange participants could design products most appropriate for target groups or adhere to the operating models of individual State Exchanges. The risk they face is that the regulation and demands vary across States. This places barriers to operational efficiencies across Health Benefit Exchanges.

On the contrary, Federal Exchange participants operate in specific States that do not have their own exchanges. They will have to adhere to Federal Exchange requirements.

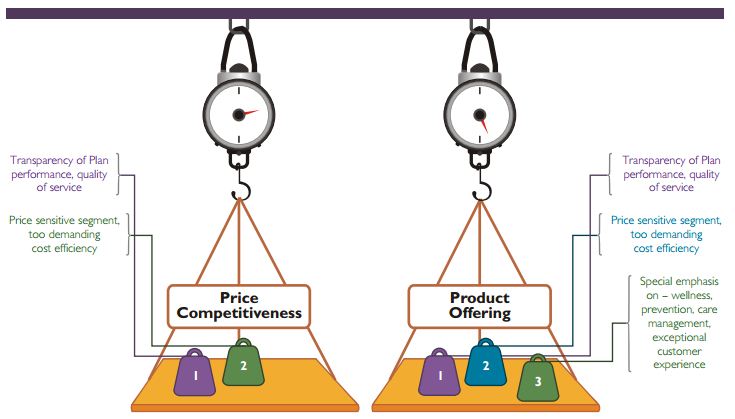

Regardless of how they operate, it is apparent that products of the health plans will have to be broadly standardized for segments. The outcome of standardization will be commoditization. As a result, product differentiation is less, leading to challenges in premium pricing. This lack of differentiation has a straightforward implication according to Porter's Generic Strategy. Cost leadership will hold the key to success to gain a competitive advantage. However achieving Cost leadership is difficult.

Cost leadership is attainable through lean and automated next-generation internal capabilities and the simplicity of the products offered. However in this case, the business model in itself lacks the ability to create value. Ideally, exchange participants need to focus on higher administration efficiencies, target products at micro segments, deliver innovative care management and superior customer experience in addition to creating an interoperable business-aligned architecture.

The Winning theme for health plans should be to transform themselves into a consumer enabled service as explained below

Win Themes for the Exchange Business

What are some of the key win themes that can generate business value?

Health Plan Situation Analysis (As-is):The Need for Business and IT Transformation

Today's health insurance companies are not prepared to make the transition to the exchange model for a number of reasons. Without a welldefined blueprint for business and IT transformation, creating value will be a challenge. The challenges are:

Insurance companies are poorly aligned with the requirements of Health Benefit Exchanges. Can they swiftly change their products, operational processes, IT systems, business models and partnerships to position themselves as winners in the Health Benefit Exchange landscape? The ones who do are the ultimate winners.

Health Plan Business Case Model: Vast Gaps to be bridged by Business Blueprint

The journey from current state to the necessary “To-be” state underlines the key success criteria for a business blueprint:

The Core Strategic Themes of To-be State are

1. Understand customer segments and drive focus to each segment

2. Gain cost leadership through low cost operations and automation

3. Use analytics and single view of stakeholder experience

4. Influence through collaboration with State agencies

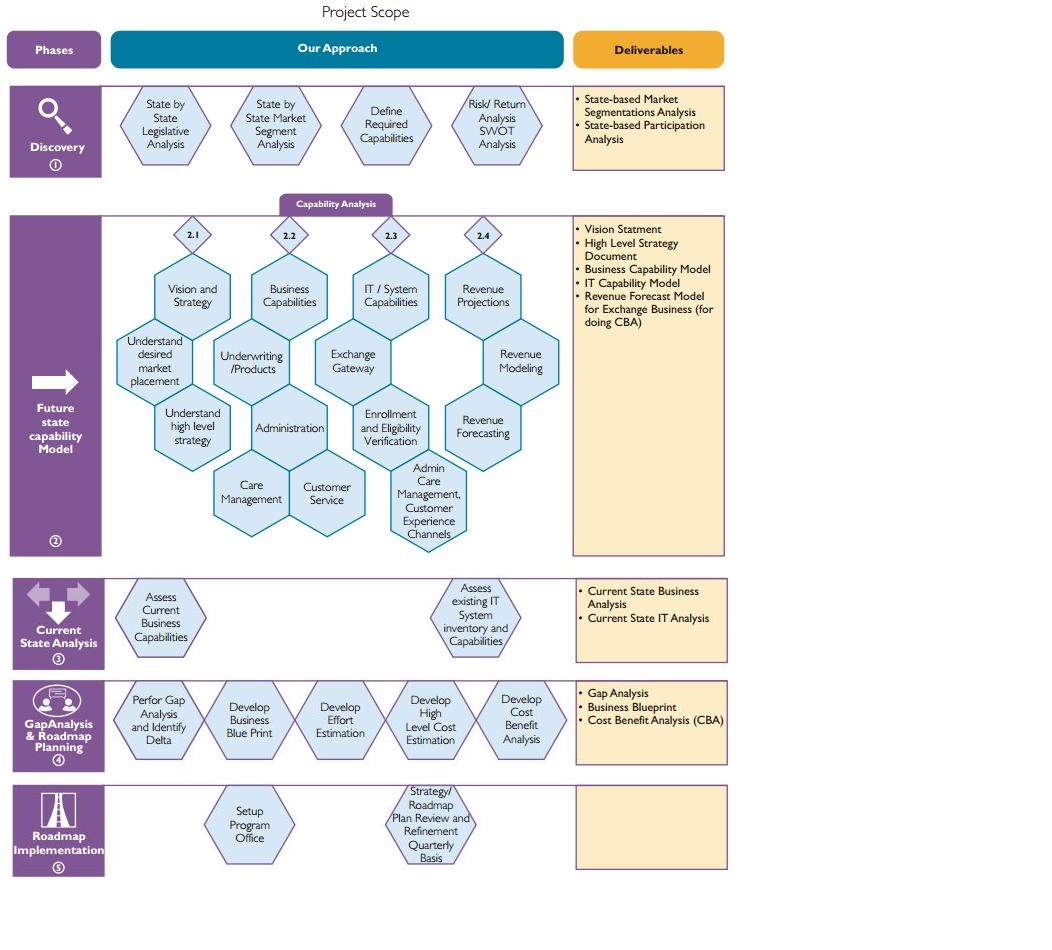

Wipro's Methodology for Creating a Business Blueprint:

Wipro's methodology for designing a business roadmap begins by creating a State by State understanding of legislation, market segments and a risk/return analysis. The central question that needs a convincing and detailed answer is, "What are the best identified choices? What is the range of future capabilities required to ensure success for the choices made?" Given the desired target position, what should the high level Health Benefit Exchange strategy be? A winning, ready-to-execute strategy is an outcome of the vision presented by leadership. Once the vision is articulated, it has to be proficiently translated into business capabilities (underwriting, product development, care management, customer service) and a heightened retail focus around the target Health Benefit Exchange segment.

Blueprint Methodology

How do we get there from here?

The delivery of business capabilities could well hinge on the role IT plays in integration with external parties, customer service systems, the plan for retail and patient centric systems, how the plan to significantly increase auto-adjudication rates is defined, how synchronized and real-time pricing/ underwriting capabilities are identified and the increased use of analytics to create insight and efficiencies.

The Health Benefit Exchange opportunity before health payers can transform business. Payers should leverage the opportunity calls for a close examination of regulatory requirements that help create a best-fit and faster go-to-market strategy.

Medical information is representative of complex relationships which often mislead practitioners to provide a holistic and comprehensive patient guidance.Semantic Networks however,simplify the process to aggregate,organize and disseminate professional knowledge for effective diagnosis and treatments possible.

Integrated care management promises great benefits for patients, providers and payers, but requires disciplined planning and execution.

Read about how Health plans can improve financial performance and health outcomes by integrating member information across the enterprise.

Locations

Locations