Banks encourage customers to increase credit and debit card usage and reduce cash transactions. The reasoning behind this is simple - banks earn interchange fees when customers use debit or credit cards, whereas, cash transactions bring no interchange revenue, on the contrary, banks incur a cost on cash transactions (due to ATM transaction and infrastructure costs).

Interestingly, it has been observed that consumers spend more when they purchase with credit or debit cards. Merchants* that encourage customers to pay by card by offering incentives are likely to see higher spends. Thus, merchants can benefit from increased sales and customer satisfaction through promotions and electronic payments. By encouraging card usage, banks and merchants can drive mutual benefits with increased spend frequency and revenue.

The banking industry can explore opportunities with partners (merchants) by understanding the potential of collaborations in Analytics. Banks with partner merchants can do magic by sharing information and harnessing the power of analytics to counter the competitive environment and give better deals to customers. On the one hand, it can increase sales for merchants and on the other, it can lead to high usage of banks’ electronic cards.

Banks and merchants have high volumes of data available that can be used to gather relevant information about their respective customers. This gives them deeper insights on customer needs, which in turn helps them to cater to customers proactively. Merchants can share sales and transactions data periodically and enable banks to analyze and understand the buying patterns and spending habits of their customers using advanced analytics techniques. Based on the analytics outcomes shared by the bank, merchants and bank, separately or collectively, can roll out offers to customers and drive campaigns. The objective of making banks’ cards more relevant and valuable to consumers is enabled with this effort. Also, as an outcome of proactive engagement, consumers can get best deals on their desired products and services, which results in higher levels of satisfaction.

* Merchants include Retailers, Eateries, etc. (Both Online and Physical)

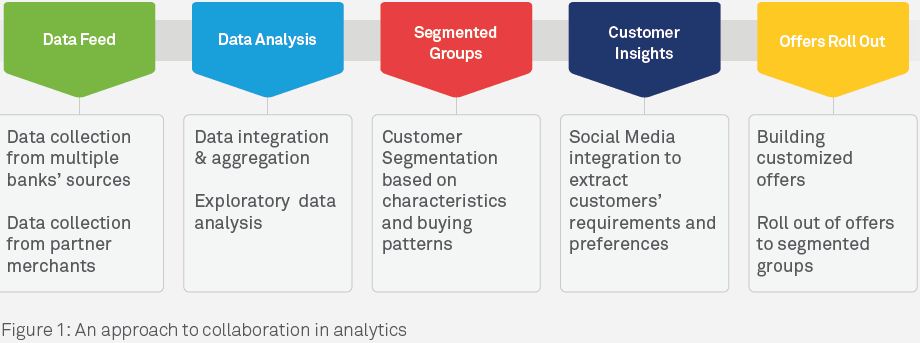

The power of alliances and analytics

A mutually-beneficial collaboration between banks and merchants can bring in a marked difference to their customer engagement efforts and also lead to better business outcomes. It is essential for financial institutions to analyze account and card holders to develop deeper insights on their usage of cards. And, data from the merchants play a crucial role in understanding customers’ payment behavior, spending habits and lifestyle. These help in creating more meaningful segments of customers based on characteristics. Using the insights gained through exploratory data analysis, these segments can help in implementing personalized and cost-effective marketing strategies. (See Figure 1)

It is essential to adopt an effective approach for building trusted relationship with customers and maximizing business outcomes using data and insights from partners. The combined effort at creating the most relevant offers can be summarized in the following steps:

1. Data Collection

Data is collected and integrated from multiple sources. Banks do have data repository of their customers that includes customers’ demographic data and transactional data. Banks can collate insightful data from their alliance partners.

2. Extracting Insights from Data

Bank’s data along with data received from merchants is integrated and aggregated by writing scripts in programming languages like R, python, databases and SQL etc. to extract meaningful insights of all types of customers. By analyzing customers using exploratory data analysis, univariate analysis and multivariate analysis, deeper understanding of consumers’ habits, needs and spend preferences can be identified. Understanding the debit and credit card customers through their past spending behavior and spending capabilities is the key to developing an effective marketing strategy.

3. Segmentation

Segmentation is an unsupervised learning technique that can help banking systems identify and categorize customers based on their preferences, buying patterns, and spending habits. Providing lucrative incentives at the right time can help increase cards usage. Segmentation can also help in reducing campaign cost by eliminating customers that should not be targeted. Using the combination of statistical segmentation and business rule, next best opportunities can be identified where the customer is more likely to spend more.

4. Social Media Integration

Business analytics can integrate available information of demographics, transactions, customer capacity and behavior with the social media into a more comprehensive customer profile. This can be achieved by merging social media data insights with the bank’s and merchant’s data. Social media and internet data can be used to determine the customer’s interest, inclination, brand perception, complaints and satisfaction level across different products and merchants. Social media can play a vital role in getting a deeper understanding of the customer in order to refine marketing strategy.

5. Building Offers

It is essential to make a relevant offer to the right person at the right time based on the defined target groups, products and services. An effective and lucrative offer will make the customer purchase more using bank cards since offers would be tagged to cards. Eg. an offer is built for a target group based on insights - if they buy groceries from a particular retailer in the first week of the month by using bank’s card, an additional discount or cashback can be given. Multiple type of promotions and offers can be rolled out to different sets of customers.

Analytics solutions are generally adopted in isolation by different sectors. Banks are yet to explore the endless possibilities with analytics in collaboration with merchants. They need to understand the benefits and scope for business growth with this kind of collaboration and do the needful to make this possible. This association will not only help banking and merchants to increase sales and cards usage but also benefit customers to get the best deals for the products and services that they look for.

Dr. Rajashekhar Karjagi has about 15 years of experience in market research, customer-driven analytics and statistical modeling. He has published more than 25 research papers, has one copyright and has conducted more than 150 analytics training sessions.

Manish Jindal has over 11 years of experience in implementing advanced analytics, statistical modeling, data mining, and BI solutions for leading clients across diverse industries like Insurance, Retail, Human Resources, and Learning Management System.