A Critical Moment for Insurers

The insurance industry is at an inflection point. Rising customer expectations, advances in AI, and the rapid growth of the insurtech ecosystem are forcing insurers to fundamentally rethink how they operate — not just at the edges, but at the core.

The pressure is real and compounding. Customers now expect seamless digital experiences as standard. Competitors — including digitally native challengers — are raising the bar on speed, personalization, and service. And regulators are adding complexity faster than most legacy platforms can absorb. The insurers pulling ahead aren't necessarily the largest or most established. They are the most adaptable.

At the heart of this adaptability is a shift in architecture: from monolithic, closed systems to modular, API-first platforms that allow capabilities to be plugged in, swapped out, and scaled without overhauling the entire stack.

Why the Pressure to Change Is Intensifying

Several converging forces are accelerating the need for transformation.

- Customer experience has become a competitive differentiator. Insurers like USAA and Lemonade have demonstrated that intuitive, digital-first interactions drive loyalty and reduce churn. The bar for what "good" looks like has moved permanently.

- The insurer's role is evolving — from payer to partner. Leading carriers are moving beyond transactional relationships, offering proactive risk management, wellness incentives, and personalized guidance. This isn't just a marketing shift; it requires fundamentally different operating capabilities.

- Cloud and AI are now table stakes. What were once differentiating capabilities are now baseline infrastructure choices. Real-time data flows, AI-driven underwriting, predictive claims management — these are no longer future-state ambitions. They are operational requirements for staying competitive.

- Insurtech integration is reshaping the value chain. Rather than building every capability in-house, forward-thinking insurers are assembling ecosystems of specialized partners — from telematics providers and fraud detection platforms to digital onboarding and embedded insurance solutions.

Underlying all of this is a structural reality: insurers have relatively few direct touchpoints with customers. Every interaction — a quote, a renewal, a claim — is a high-stakes moment. Getting these right requires systems that are fast, flexible, and deeply integrated.

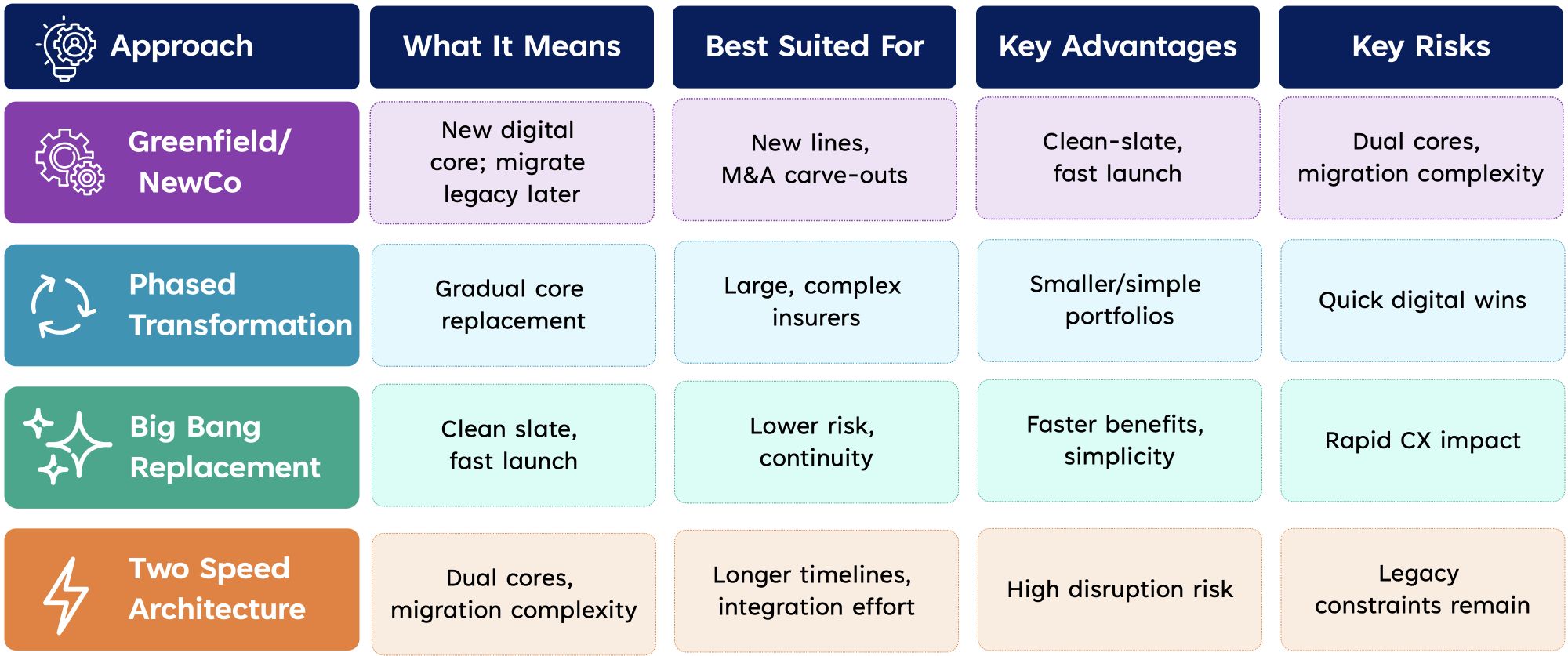

The Constraints Holding Insurers Back

Even insurers who have modernized parts of their technology stack face persistent friction. The most common obstacles aren't technical in isolation — they are structural.

Many carriers are managing multiple core systems accumulated through acquisitions and organic growth, with policies scattered across platforms and integration becoming increasingly complex. Others find that even relatively modern cores struggle to connect with today's insurtech solutions and emerging technologies. Operational efficiency pressures are intensifying, while skill gaps in heavily customized legacy environments make maintenance increasingly difficult and expensive.

Perhaps most consequentially, new business models — particularly embedded insurance and usage-based products — demand a level of speed and modularity that traditional architectures simply weren't built to support.

Modernization, in this context, isn't just a technology decision. It's a business viability imperative.