Gen Z’s Credit Gap: A Digital Dilemma

By 2030, Gen Z will represent a third of the global workforce, commanding trillions in spending power. Yet, despite their economic potential, credit card adoption among this cohort remains alarmingly low. According to TransUnion, only half of Gen Z adults in the U.S. hold a credit card, compared to nearly three-quarters of Millennials. This disparity signals that traditional credit models are failing to resonate with a digitally native, trust-conscious, and financially cautious audience.

Card issuers are at a critical juncture. The decline in credit card usage is affecting not only fee and interest income but also poses risks to sustaining long-term customer relationships. To stay competitive, issuers must re-evaluate their strategies, product offerings, and engagement approaches, beginning with a thorough understanding of Gen Z’s distinct financial behaviors and expectations.

Four Key Reasons for Gen Z's Limited Credit Card Use

Gen Z’s low credit card adoption is driven by the following core factors:

- Digital-First Mindset

Gen Z gravitates toward frictionless digital payments like Apple Pay, Venmo, and BNPL. Speed and convenience matter more than traditional security features. - Financial Literacy Gaps

Confusion around billing, interest, and charges leads to anxiety. Many struggle with late payments and understanding statements. - Split-Brain Budgeting

They separate spending: debit for daily essentials, credit for big-ticket items. Peer-to-peer apps make cost-sharing easier than credit cards. - Instant Gratification Over Loyalty

Traditional loyalty programs don’t resonate with Gen Z. Simpler, instant-benefit options like debit and BNPL win out over complex reward systems. While 17% of Gen Z users redeem rewards monthly, overall credit card adoption remains low compared to older generations (39% vs. 51%).

Encouraging Gen Z to Use Credit Cards

To engage Gen Z and boost credit card adoption, banks must rethink their approach and align with Gen Z’s digital-first expectations. Banks should embed digital account opening within student portals to enable seamless access to savings accounts and tuition payments during class registration. An Artificial Intelligence (AI)-first digital experience is essential; platforms must be optimized for agentic commerce and deliver personalized offers with frictionless onboarding.

Product design must resonate with Gen Z’s financial journey, including budgeting apps, linked credit cards for young adults, real-time account opening, parental controls, and relevant loan options such as student loan refinancing and rental or auto loans. Financial literacy support is critical, with interactive, personalized advice and real-time insurance or refund disbursements via debit cards. Customizing solutions for Gen Z segments, students, gig workers, and new workforce entrants, ensures greater engagement.

Highlighting credit card benefits such as rewards, credit history building, and extra protection (dispute rights, insurance) is essential. Banks must actively educate users on credit card fundamentals, including billing cycles, interest rates, fees, and repayment strategies. Simultaneously, they should design cards for specific needs, such as co-owned cards, secured cards with 0% Annual Percentage Rate (APR), and alternative underwriting models. Embedded payment solutions within Gen Z’s preferred digital environments make conversion from app users to card users easier, offering both convenience and efficiency.

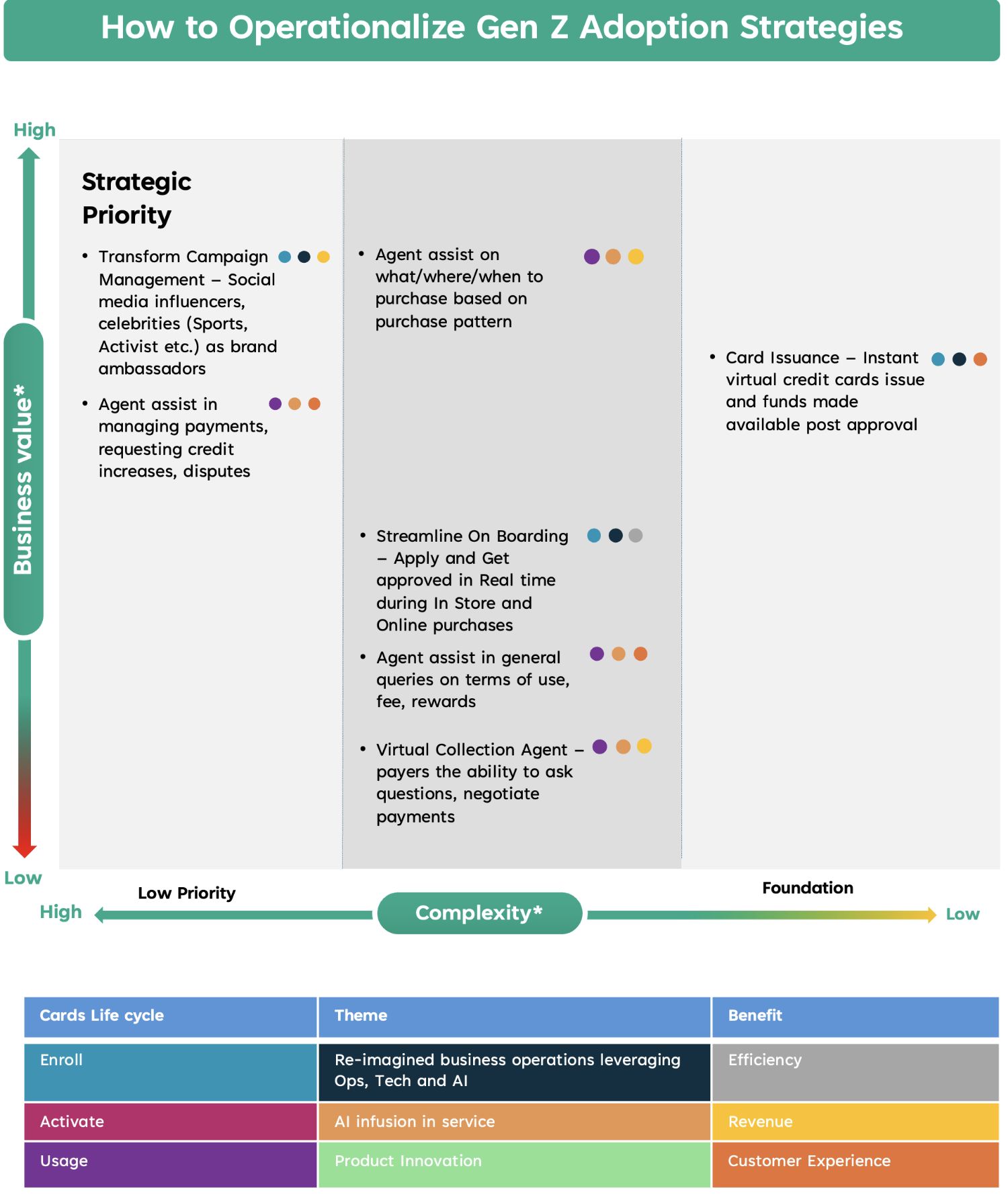

Top Use Cases to Boost Gen Z Credit Card Adoption

The strategic priorities for card issuers in attracting and retaining Gen Z customers revolve around three key dimensions: Growth, Efficiency, and Experience. Each dimension highlights where AI investments can deliver the greatest impact across revenue generation, cost optimization, and customer experience enhancements in the evolving payments landscape.