The banking and financial services industry is at a critical inflection point. Years of digital transformation, combined with rapid advances in artificial intelligence, have fundamentally reshaped how value is created and delivered. Simultaneously, traditional revenue streams are under pressure as fee-based income models weaken, margins tighten, and digital-native competitors redefine customer expectations with unprecedented speed.

In the next three years, BFSI institutions that use AI only for cost-saving will be outpaced by those leveraging it as a revenue driver through data monetization in Saudi Arabia’s digital economy. Fintechs are integrating intelligence into their offerings, raising standards for personalization and agility. Now, financial institutions must turn fragmented data into business value; relying solely on cost efficiency won’t suffice. As competitors adopt AI-driven models, effective data monetization has become essential.

By leveraging advanced analytics, machine learning, and generative AI, BFSI institutions can unlock new revenue streams, improve operational efficiency, and deliver the hyper-personalized experiences that deepen customer loyalty.

Why Data Monetization is a Strategic Imperative

Data monetization in banking is moving from experimentation to scale. The global Data Monetization for Banks market size reached USD 3.85 billion in 2024, with a robust compound annual growth rate (CAGR) of 17.2%. The sector is on track to expand significantly, with the market forecasted to reach USD 15.52 billion by 2033.

Several forces are accelerating this shift: customers increasingly expect personalized financial services, regulators are encouraging open banking, and a surge in fintech investment, which reached approximately $180 billion in 2023, is intensifying competitive pressure.

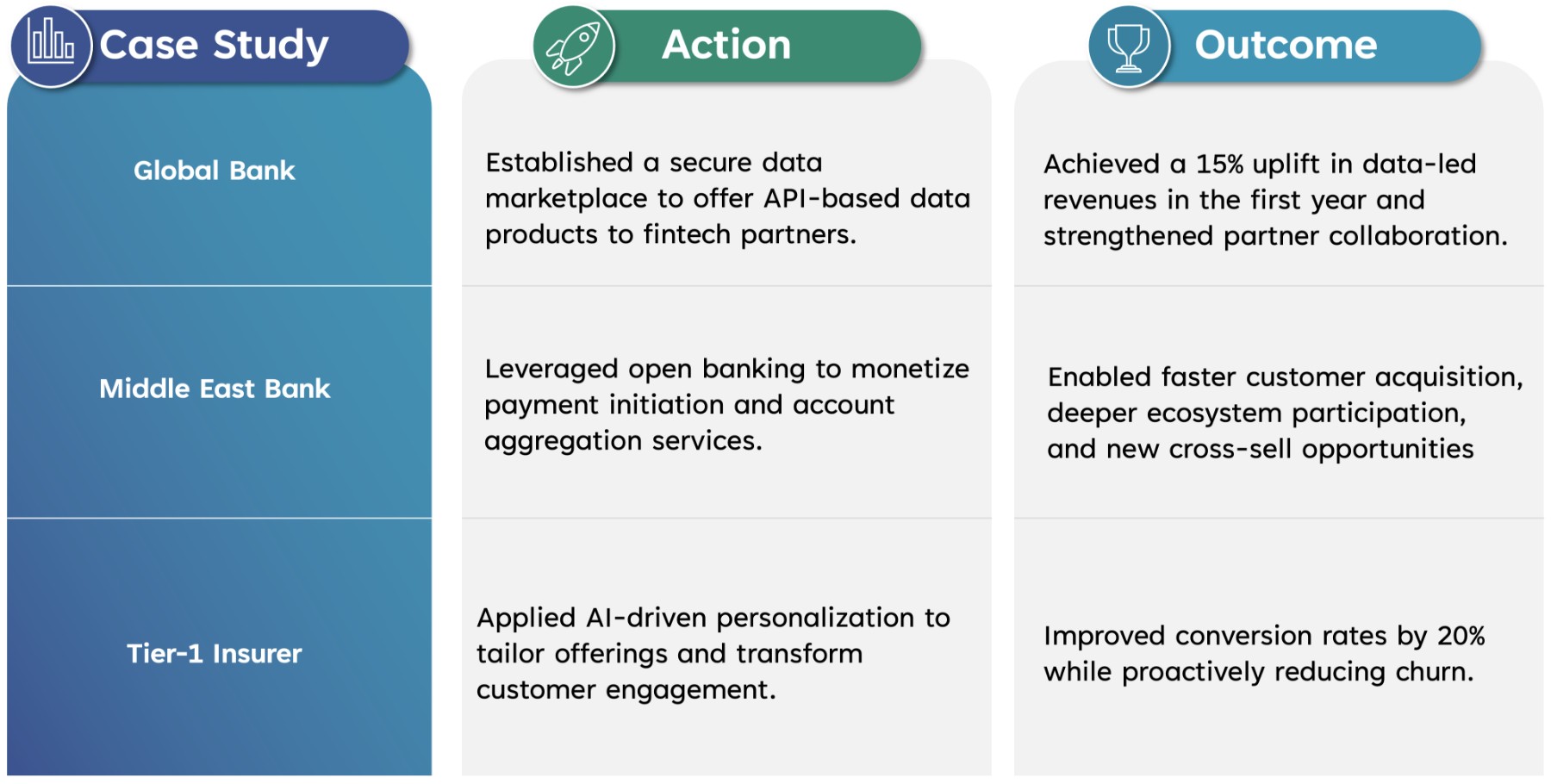

There are three primary monetization pathways:

- Revenue Uplift (cross-sell, personalization, embedded finance)

- New Revenue Lines (APIs, insight-as-a-service, ecosystem fees)

- Cost Avoidance with Revenue Impact (fraud reduction tied to margin protection)

Institutions that fail to monetize data risk losing relevance. Conversely, effective monetization enables diversification beyond traditional fee income, strengthens customer engagement, and builds long-term resilience. The opportunity spans both internal and external use cases, from AI-driven fraud detection to Data-as-a-Service models that monetize anonymized insights and embedded financial intelligence.